As US households increasingly shift towards online content platforms, a quarter of US Internet users now rely on a mix of advertising-funded video on demand (AVoD) and subscription video on demand (SVoD) services for their entertainment. This figure has risen from 15% in Q1 2020. Ampere’s latest catalogue data reveals the differing strategies between AVoD and SVoD services when it comes to exclusive content.

The quality and popularity of SVoD services is typically driven by their exclusive titles whereas AVoD services tend to rely on high volumes of non-exclusive content from major studios to bolster their quality perception of their catalogues. Ampere’s analysis demonstrates the potential for AVoD services to co-exist with well-established subscription services and offer a cheaper way to view content online for price-sensitive consumers.

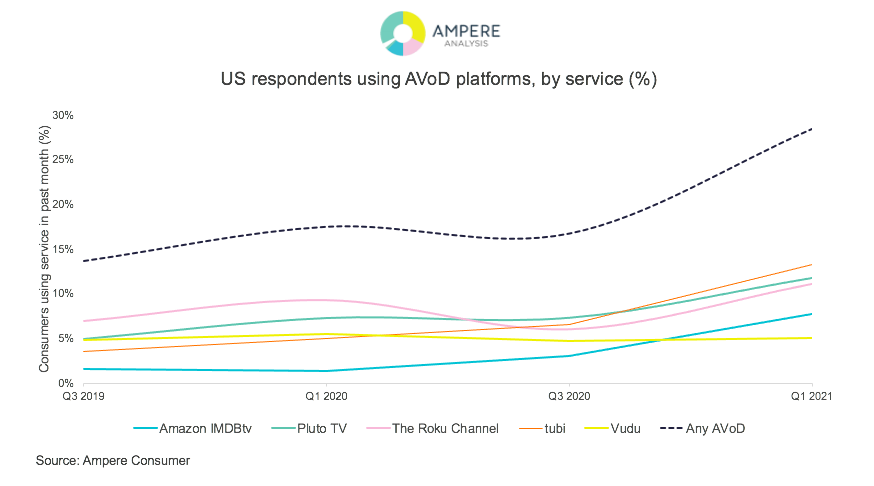

The US AVoD viewer and content

AVoD viewers tend to be older and less affluent than their SVoD counterparts and tend not to stack multiple SVoD services, preferring traditional pay TV packages. In the study, older users (age 55-64 years old) were the fastest growing age bracket of AVoD viewers, with a 7% increase in AVoD uptake among the group in the last year alone. This was also the fastest growing age bracket for SVoD but due to the greater maturity of the SVoD market, saw just a 3.5% growth in the last year.

Tom Bell, analyst at Ampere Analysis, said: “We can see the appeal with older audiences at present, but AVoD services will need to compete more directly with the content on SVoD if they want to attract the younger, more affluent audience already familiar with SVoD.”

US AVoD catalogues are large - but are primarily made up of older, non-exclusive titles. While SVoD services typically rely on their vast catalogue of exclusive titles to increase the quality and popularity of their content offering, this is not the case for AVoD services. The quality and popularity of AVoD catalogues is driven mainly by non-exclusive content, with their large catalogues made up of a much higher proportion of titles from studios which are also licensed to other services.

The AVoD/SVoD crossover

All major SVoD services in the US offer some content that is available on AVoD for free. Amazon, Hulu and Peacock have a significant amount of content that is also available via AVoD services. In total, 12% of titles on SVoD are also available on a free AVoD platform in the US. However, a small number of platforms account for the majority of the overlap between SVoD and AVoD. Amazon Prime Video has the greatest overlap with Fox-owned AVoD service Tubi, with 6600 titles shared between the two services; over 90% of these are lower-value movie content. This is followed by NBCU-backed Peacock, with 715 titles available free on Tubi, with the majority of these also available via Peacock’s free AVoD tier.

Looking ahead, the AVoD players are starting to move into original programming to differentiate their catalogues and reduce reliance on licensed content. Roku, Vudu, Crackle and IMDb TV have all begun to commission original programming, focusing primarily on documentary and comedy titles. Rival service Tubi has also committed to original productions, targeting 140 hours of new original content in late 2021.

Tom Bell concluded: “As studios are reserving an increasing proportion of their content for their own platforms, AVoD platforms are beginning to follow suit and commission their own originals. While content exclusivity remains a key difference in strategy between AVoD and SVoD platforms, these early moves into original commissioning bring AVoD players a step closer to increasing their catalogue exclusivity and quality and differentiating themselves in a crowded market.”